Taxation of business income and specialized business activities

Unit: Advanced Taxation

Premium Topic Resources

Sign in to download the full Topic PDF and enable offline revision mode.

Login to Access

Join the community! 550+ students upgraded in the last 24 hours.

Limited Discount Seats Available

Practice CPA Advanced Taxation Taxation of business income and specialized business activities questions with detailed answers and explanations.

Access past exam questions by topic, improve your understanding, and download PDF for offline revision.

December 2025

1 Questions

Question 2b

Patrick and John are partners operating a partnership business Jomani Enterprises and sharing profits and losses

equally. The business operates through two independent branches; the head office branch in Nakuru and Kericho

branch. The partners have received a tax assessment from the Revenue Authority with a taxable income of

Sh.684,000 each for the year ended 31 December 2024. They have provided the following details to help in

responding to the tax assessment:

| 1. | The following balances were extracted from the books of the partnership on 31 December 2024

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2. | Kericho branch sells goods transferred from head office at cost. However, it is allowed to make purchases from other suppliers and also maintain a separate bank account. During the year, no goods were transferred from the head office to the branch. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3. | All goods were sold at both head office and Kericho branch at 30% above cost. All employees were entitled to a commission at the rate of 1% of the sales during the year. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4. | Analysis of the bank statement during the year revealed the following:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5. | Head office salaries and wages include salary paid to each partner of Sh.20,000 per month. The bank loan had been taken on 1 July 2024. | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 6. | The current account balances as at 31 December 2023 were as shown below:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 7. | The partners had withdrawn goods worth Sh.520,000 and Sh.430,000 for Patrick and John respectively. The partnership deed provided for 3% interest on drawings. |

Required:

(i) Compute the taxable income of the partnership for the year ended 31 December 2024.

(ii) Compute the taxable income of each partner from the income computed in (b) (i) above for the year ended

31 December 2024.

(iii) Advise the partners in relation to the assessment issued by the Revenue Authority.

August 2025

3 Questions

Question 3b

Western Mining Ltd. is a company involved in the exploration and extraction of gold and other precious minerals in

Kakamega County. The following is the statement of profit or loss and other comprehensive income for the year

ended 31 December 2024:

| Western Mining Ltd. Statement of profit or loss and other comprehensive income for the year ended 31 December 2024 |

| Sh.“000” | Sh.“000” | |

| Revenue (export of goods) | 600,000 | |

| Cost of sales: | ||

| Extraction costs (labour, fuel, blasting, water) | (220,000) | |

| Depreciation - Mining equipment | (50,000) | |

| Royalties paid to Ministry of Mining (4% of sales) | (24,000) | |

| Site restoration provision | (10,000) | |

| Gross profit | 296,000 | |

| Operating expenses: | ||

| Salaries and wages | 40,000 | |

| Administration and head office expenses | 30,000 | |

| Amortisation of exploration license | 8,000 | |

| Impairment loss on mine development assets | 6,000 | |

| Legal fines for environmental violations | 2,000 | |

| Advertising and marketing expenses | 5,000 | (91,000) |

| Operating profit | 205,000 | |

| Finance costs (interest on loan from bank) | (10,000) | |

| Tax expense | (58,500) | |

| 136,500 | ||

| Other compressive income: | ||

| Revaluation gain on freehold mining land | 20,000 | |

| Exchange loss on translation of foreign operations | (3,000) | |

| Total comprehensive income | 153,500 |

Additional information:

- The company incurred Sh.15,000,000 in construction of roads within the mining site and Sh.12,000,000 in acquiring drilling equipment during the year.

- The exploration license is valid for 4 years commencing 1 January 2023.

- The site restoration provision is based on an estimated costs to be incurred in year 2025.

- The company made a donation of Sh.3,000,000 to a local school project (not approved by the cabinet secretary). This amount was included in administration and head office expenses.

- The company claimed revaluation gain on freehold land on equity but did not sell or dispose of the land.

- The legal fine resulted from non-compliance with environmental regulations under the Mining Act.

- Deprecation was computed using International Financial Reporting Standards (IFRS) rules and not aligned with investment allowances under the Income Tax Act.

Required:

(i) Prepare statement of adjusted taxable profit or loss for Western Mining Ltd. for the year ended

31 December 2024.

(ii) Determine the corporate tax, if any, payable by the company for the year ended 31 December 2024.

(iii) Identify TWO obligations of mining companies operating in Kenya under the Income Tax Act.

Question 1a

You have been appointed as a tax advisor to a contractor involved in infrastructure projects for a County

Government. The contractor has recently received conflicting tax assessment from both the Revenue Authority

relating to withholding tax and County Government relating to contractual service levy. The contractor believes the

charges are duplicative and not grounded in clear provisions. The delays in resolving the dispute have stalled

payments and strained the contractor’s cash flows.

Required:

(i) Explain the tax dispute resolution mechanism available to the contractor under Kenyan tax laws.

(ii) Advise the contractor on the steps to take in resolving the tax dispute with the Revenue Authority and

County Government.

(iii) Propose FOUR institutional reforms that the County Government could implement to avoid similar tax

disputes with contractors in the future.

Question 4c

Robert Mwema is a senior software engineer at Steel Ltd. and has provided the following details for the year ended

31 December 2024:

- His gross monthly salary is Sh.250,000 which includes a house allowance Sh.70,000 per annum.

- He owns 15% shares in Innovatech Ltd., a private consulting company where he receives annual dividend of Sh.600,000.

- He resides in a house he purchased through a personal loan of Sh.1,500,000 obtained from a bank on 1 September 2023 at an interest rate of 14% per annum repayable over 8 years.

- He contributes Sh.18,000 per month to a Sacco investment account towards his retirement.

- He has taken a ten-year education insurance policy where he contributes Sh.3,500 per month for his two children’s university education.

- Robert Mwema has invested Sh.6,000,000 in a fixed deposit account and 15-year government infrastructure bond on equal basis both earning an annual interest at the rate of 12%.

- He also owns a rental apartment, which generates monthly rental income of Sh.80,000 but incurs annual maintenance expenses of Sh.120,000 and county land rates of Sh.24,000.

Required:

Advise Robert Mwema on tax planning strategies that he could implement to optimise his tax position and

legally minimise his annual tax liability from the information provided above.

Support your argument with relevant

computations where necessary.

April 2025

1 Questions

Question 2b

Ryan and Michael are in a partnership business trading as RAM Enterprises and sharing profits and losses in the

ratio of 3:2 respectively.

The following details relate to the business for the year ended 31 December 2024:

| Sh. | |

| Capital account (1 January 2024):Ryan | 4,000,000 |

| Capital account (1 January 2024):Michael | 3,200,000 |

| Sh. | |

| Current account (31 December 2024):Ryan | 600,000 (Credit) |

| Current account (31 December 2024):Michael | 900,000 (Credit) |

| Inventories as at 1 January 2024 | 6,203,000 |

| Non-current assets | 4,200,000 |

| Trade receivables | 1,800,000 |

| Trade payables | 642,000 |

| Cost of sales | 2,469,860 |

| Transport costs | 713,000 |

| Interest on business loans | 390,000 |

| Drawings of goods at selling price:Ryan | 2,250,000 |

| Drawings of goods at selling price:Michael | 2,400,000 |

| Bank | 373,000 |

| General expenses | 684,500 |

| Salaries | 2,722,020 |

| Rent | 3,000,000 |

| Electricity | 364,000 |

| Depreciation | 464,000 |

| Net interest income (Mali Ltd.) | 200,000 |

Additional information:

| 1. | Current account balances were extracted after preparing the final accounts of the partnership for the year ended 31 December 2024. |

| 2. | Sales are made up of 200% of the share of the total profits by the partners and include value added tax (VAT) at the rate of 16%. |

| 3. | Interest on drawings was charged at 10% on the partners drawings and interest on capital was at 5% per annum. |

| 4. | Salaries include partners’ salary amounting to Sh.880,260 and Sh.760,260 to Ryan and Michael respectively. The partners salaries were included in the current account balances as at 31 December 2024. |

| 5. | Rent accrued was Sh.120,000 at year end and there was a prepayment of rent Sh.40,000 at the beginning of the year. Electricity owing as at 1 January 2024 was Sh.150,000. |

| 6. | On 2 September 2024, the business ordered for goods costing Sh.225,000 which were recorded as purchases but were never received as they were stolen while in transit. The transporter later accepted liability and paid a compensation in January 2025 of Sh.200,000. No adjustments had been made in the books in respect of the loss or claim as at 31 December 2024. |

| 7. | Non-current assets were acquired in the month of January 2024 and comprised the following: |

| 7 | Sh. | |

| Computers | 240,000 | |

| Office partitions | 300,000 | |

| Furniture | 120,000 | |

| Saloon vehicle | 2,460,000 |

| 8. | There were no opening balances in the current account of partners. |

Required:

(i) The partnership taxable profit or loss for the year ended 31 December 2024.

(ii) Taxable income of each partner.

December 2024

1 Questions

Question 1b

Kamaly and Kalangi have been trading as Kaka Enterprises. The entity had reported a net profit of Sh.484,900.

However, the reported profit was disputed by the revenue authority during the year of income 2023. The assessed

taxable profit for the partnership by the revenue authority was Sh.3,880,000.

The partners have provided the following details to assist them prepare for an adjusted taxable profit which would

assist in determining whether the assessment by the revenue authority was fair:

| Receipts and payments (Bank account) | |||

| Sh. | Sh. | ||

| Balance brought forward 1 January 2023 | 1,840,000 | Cash purchases | 500,000 |

| Receipts from debtors | 3,600,000 | Payments to creditors | 1,890,000 |

| Cash sales | 720,000 | Electricity | 188,000 |

| Sale of motor vehicle | 360,000 | Telephone | 172,000 |

| 15% bank loan | 400,000 | Purchase of furniture | 350,000 |

| Balance carried forward | 960,000 | General expenses | 3,700,000 |

| Salaries and wages | 480,000 | ||

| Office computers | 180,000 | ||

| Rent expenses | 240,000 | ||

| Insurance | 96,000 | ||

| Advertising | 84,000 | ||

| 7,880,000 | 7,880,000 | ||

Additional information:

| 1. | The partners contributed capital of Sh.400,000 and Sh.600,000 for Kamaly and Kalangi respectively which was included in the opening balance in the receipts and payments account. |

| 2. | General expenses included the following items which were debited in the statement of profit and loss account: |

| 2 | Sh. | |

| 90,000 | |

| 300,000 | |

| 350,000 | |

| 32,000 | |

| 48,000 | |

| 200,000 | |

| 82,000 | |

| 1,200,000 | |

| 742,000 | |

| 200,000 | |

| 96,000 | |

| 360,000 |

| 3. | Other details included: | ||

| 1 January 2023 Sh. | 31 December 2023 Sh. | ||

| Creditors for goods | 550,000 | 1,460,000 | |

| Debtors for goods | 640,000 | 820,000 | |

| Salaries and wages accrued | 120,000 | 89,000 | |

| Rent expenses prepaid | 36,000 | 24,000 | |

| Office computers | 150,000 | 240,000 | |

| Inventories for goods in trade | 192,000 | 120,000 | |

| Cash at bank | 840,000 | 960,000 |

| 4. | Salaries and wages included salaries paid to domestic workers for partners amounting to Sh.96,000. |

| 5. | Total sales and purchases for the year 2023 were undercast by 20%. |

| 6. | The 15% bank loan of Sh.400,000 relates to repairs to private residence of Kalangi. |

| 7. | Telephone expenses amounting to Sh.60,000 related to partners personal calls. |

| 8. | Rent expenses were understated by 25%. |

Required: | |

| (i). | Prepare a revised statement of adjusted profit or loss for the partnership business. |

| (ii). | Advise the partners in relation to the assessed profit by the revenue authority as compared to the adjusted taxable profit obtained in (b) (i) above. |

August 2024

1 Questions

Question 5a

Evaluate FOUR ethical issues that policy makers are required to consider when designing tax systems.

April 2024

1 Questions

Question 1b

The following information was extracted from the books of Henry and Titus who operate a partnership business and

share profits and losses in the ratio of 3:2 respectively:

| 1. | An extract from the statement of financial position as at 31 December 2022 revealed the following information about the partnership: |

| 1. | Asset | Cost/net book value | Sh.“000” |

| Freehold land | Cost | 64,000 | |

| Office equipment | Net book value | 4,160 | |

| Furniture and fittings | Net book value | 4,800 | |

| Delivery vans | Net book value | 8,000 | |

| The net book values as at 31 December 2022 were the same as the tax written down values. | |||

| 2. | Current assets and liabilities as at 31 December 2022 were reported as follows: |

| 2. | Sh.“000” | |

| Stock | 8,800 | |

| Trade receivables | 640 | |

| Bank overdraft | 480 | |

| Cash in hand | 64 |

| 3. | On 1 January 2023, each partner contributed additional capital of Sh.5,000,000. Interest on capital was at the rate of 5% per annum. |

| 4. | Sales proceeds that were banked in the year amounted to Sh.160,000,000. The accountant had paid the following expenses from sales proceeds before banking the balance: |

| 4. | Sh. | |

| Office rent | 32,000 per month | |

| Office expenses | 8,000 per week | |

| Laptop for office use | 40,000 | |

| Salaries and wages - casual workers | 3,600 per week | |

| Carriage outwards | 5,200 per week | |

| Salary to partners: Henry | 16,000 per month | |

| Salary to partners: Titus | 24,000 per month |

| 5. | From the bank, the partnership made the following payments: |

| 5. | Sh. | |

| Purchase of computers | 102,400 | |

| Purchase of motor cycle for salesmen | 160,000 | |

| Staff salaries per month | 80,000 | |

| Purchase of goods for resale | 124,800,000 | |

| Drawings per month: Henry | 80,000 | |

| Drawings per month: Titus | 64,000 | |

| Drawings per month: Stellah | 36,000 | |

| Bank charges per month | 2,400 | |

| Telephone bills per month | 6,400 | |

| Electricity bill per month | 8,000 |

| 6. | On 1 September 2023, Stellah was admitted as a partner on the following terms:

|

| 7. | Analysis of other records revealed the following:

|

| 8. | Partners’ capital as at 1 January 2023 was contributed equally by Henry and Titus. |

| Assume a 52 weeks year. | |

Required: | |

| (i) | Prepare a statement showing the taxable profit or loss of the partnership before and after admission of Stellah for the year ended 31 December 2023. |

| (ii) | Allocation of the profit or loss computed in (b) (i) above to the partners. |

December 2023

1 Questions

Question 1b

Asili and Tulivu established a partnership business sharing profits and losses in the ratio of 3:2 respectively. The

following statement of profit or loss of the business for the year ended 31 December 2022 was provided:

| Sh. | Sh. | |

| Sales | 20,184,000 | |

| Gain on sale of shares | 1,056,000 | |

| Foreign exchange gain-unrealised | 450,000 | |

| Recovery from insurance on stolen stock | 1,400,000 | |

| Discount received | 552,000 | |

| Dividend - Wakaguzi Co-operative Society (gross) | 153,000 | |

| Total incomes | 23,795,000 | |

| Expenses: | ||

| Purchases | 8,526,000 | |

| Purchase of computers | 540,000 | |

| Partners salaries | 2,160,000 | |

| Legal fees | 2,040,000 | |

| Repairs and maintenance | 1,705,200 | |

| Rent and rates | 733,800 | |

| Interest on loan | 498,600 | |

| General expenses | 2,892,000 | |

| Motor vehicle expenses | 2,520,000 | |

| Insurance | 468,000 | |

| Preliminary expenses | 788,400 | |

| Directors fees | 1,800,000 | |

| Audit fees | 444,600 | |

| Debenture interest | 1,080,000 | |

| Travelling expenses | 288,000 | (26,484,600) |

| Net loss | (2,689,600) |

Additional information:

| 1. | Purchases and sales of goods were inclusive of value added tax (VAT) at the rate of 16%. |

| 2. | Closing inventory was valued at Sh.5,520,000 while opening inventory was 10% of sales net of VAT. |

| 3. | The partnership was converted into a limited company by the name Asili Ltd. on 1 April 2022. |

| 4. | Income and expenses accrued evenly throughout the year unless otherwise stated. |

| 5. | Legal fees comprised: |

| Sh. | ||

| Notice for change of business name | 194,400 | |

| Conveyance fees of business premises | 217,200 | |

| Stamp duty | 349,800 | |

| Acquisition of business loan | 62,400 | |

| Recovery of bad debts | 135,000 | |

| Signing a 99 year lease agreement | 385,200 | |

| Purchase of Asili’s private residence | 450,000 | |

| Appeal against tax assessment | 246,000 | |

| 2,040,000 | ||

| 6. | Repairs and maintenance comprised: | |

| Purchase of furniture | 288,000 | |

| Installation of neon sign | 180,000 | |

| Designing office block | 1,170,000 | |

| Painting of new office block | 67,200 | |

| 1,705,200 | ||

| 7. | General expenses included: | |

| Registering of patents | 336,000 | |

| Negotiating for additional land for business expansion | 168,000 |

| 8. | Interest on loan includes interest on partners capital of Sh.300,000 which was shared according to profit and loss sharing ratio. |

Required: Prepare a statement of adjusted taxable profit or loss for the year ended 31 December 2022 for: | |

| (i). | Asili and Tulivu partnership business. |

| (ii). | Asili Ltd. Company. |

| (iii). | A schedule showing allocation of adjusted partnership profit or loss computed in (b) (i) above, to the partners. |

August 2023

5 Questions

Question 5c

Johnson Shauri has not been maintaining proper books of accounts since the inception of his business in year 2019.

The following balances were obtained from the available business records for the four year period ended

31 December 2022:

| 31 December 2019 | 31 December 2020 | 31 December 2021 | 31 December 2022 | |

| Sh.“000” | Sh.“000” | Sh.“000” | Sh.“000” | |

| Leasehold property | 11,760 | 11,760 | 11,760 | 11,760 |

| Motor vehicles | 5,040 | 4,720 | 9,360 | 10,760 |

| Furniture | 864 | 864 | 864 | 864 |

| Bank overdraft | 1,288 | 1,400 | 1,210 | 1,115 |

| Loss on sale of investment | - | 100 | - | - |

| Accounts receivable | 432 | 504 | 408 | 600 |

| Mortgage loan | 2,080 | 1,840 | 1,620 | 1,500 |

| Inventory | 620 | 572 | 482 | 520 |

| Computers | 620 | 720 | 840 | 720 |

| Bank account | 240 | 268 | 272 | 286 |

| Personal clothes and effects | 60 | 80 | 100 | 120 |

The following additional information was obtained:

- Drawings of goods and provision for taxation for the year 2019 were Sh.600,000 and Sh.360,000 respectively and has been accumulating at a rate of 10% annually.

- Capital allowances were agreed at a total of Sh.920,000 for each of the four years.

- Donations to a political party in the year 2020 amounted to Sh.142,000.

- Gifts from relatives for the year 2021 were Sh.840,000.

- Contingent liability in respect of a pending court case in the year 2022 was Sh.1,000,000.

- Rent paid on behalf of a close friend was Sh.605,000 in the year 2022.

- Living expenses were estimated at Sh.800,000 in the year 2019 and had been increasing at the rate of 15% cumulatively each year.

Required:

(i) Compute the taxable income or loss of Johnson Shauri for the three-year period ended 31 December 2020, 2021

and 2022.

(ii) Summarise THREE specific actions that a tax practitioner could undertake upon discovery of an irregularity in the

client’s business.

Question 4b

KK Realtors are in the real estate business. They rent out two prime highrise buildings, one a residential apartment

and the other an office block. They are registered for the monthly residential rental obligation as well as filing for

value added tax (VAT).

Details of their transactions for the month of December 2022 are provided below:

| Incomes | Sh.“000” |

| Rent: Apartment | 1,248,450 |

| Rent: Office block | 7,244,200 |

| Expenses: | |

| Garbage collection | 75,864 |

| Sewerage | 92,8090 |

| Repairs and maintenance (outsourced to local company) | 144,420 |

| Housing agents fee (5% of income) | ? |

| Security firm (eight day and eight night guards) | 464,000 |

| Insurance | 580,000 |

| Interest on bank loan | 139,200 |

| Caretakers’ salaries | 92,800 |

| Webhosting (by South Africa-based company) | 67,280 |

| Audit and assurance fee | 1,334,000 |

| Telephone and electricity | 52,952 |

| Other staff salaries | 992,496 |

| Architect’s fee (based in France) | 184,730 |

The following additional information is provided:

1. With the exception of housing agents fee, webhosting and architect’s fee, a quarter of the expenses relate

to the residential business while the rest relate to the office block.

2. Housing agents fee accrues based on the amount paid for income collected from each property.

3. Webhosting and architects fee could not be directly attributed to either the residential apartment or office

block.

4. Tenants of the office block are agents for withholding value added tax (VAT) and withholding rental

income.

5. The figures provided are quoted inclusive of VAT where applicable.

Required:

(i) Calculate the tax payable under the VAT and income tax obligations by KK Realtors for the month of

December 2022.

(ii) Show the withholding tax collected under the obligations in (b)(i) above, if any, as well as the net rent

income received by KK Realtors, as cash.

Question 2a

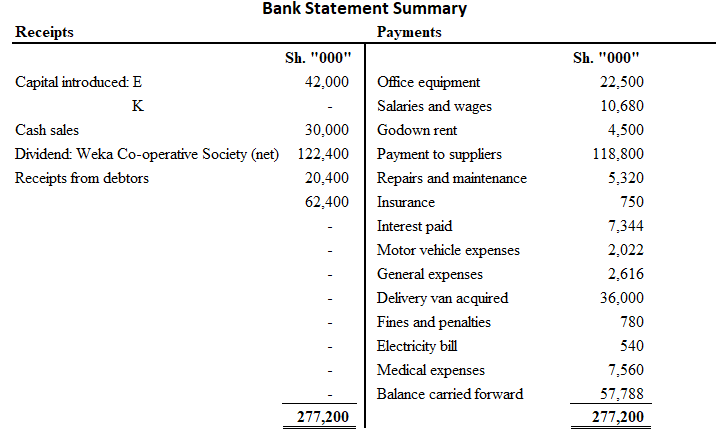

E and K commenced trading as partners under the name EK Enterprises on 1 January 2022. They share profits and

losses equally and were entitled to receive monthly salaries of Sh.240,000 and Sh.288,000 for E and K respectively.

The partnership did not maintain a complete set of accounting records. The following is a summary of the partnership’s

bank statement for the year ended 31 December 2022:

Additional information:

| 1. | As at 31 December 2022, the partnership owed suppliers Sh.9,360,000 while the amount owed by customers was Sh.10,740,000. |

| 2. | Rebate received from suppliers amounted to Sh.1,590,000 and discount allowed to customers amounted to Sh.1,416,000. |

| 3. | Bad debts amounted to Sh.984,000 out of which Sh.240,000 relate to a loan advanced to E that was overdue. |

| 4. | Closing stock was valued at Sh.7,440,000 as at 31 December 2022. |

| 5. | Salaries and wages include salary to the partners for the year. |

| 6. | Included in the interest expense is interest on partners’ capital contribution at the rate of 8% per annum. |

| 7. | The annual rent for the godown was Sh.5,400,000. |

| 8. | As at 31 December 2022, electricity and insurance owing amounted to Sh.300,000 and Sh.153,600 respectively. |

| 9. | The following payments were made in cash from cash sales before banking: |

| 9. | Sh. | |

| Motor vehicle expenses (per annum) | 1,656,000 | |

| Wages (per annum) | 1,944,000 | |

| Sundry expenses (per annum) | 420,000 | |

| Weekly drawings: E | 86,400 | |

| Weekly drawings: K | 46,800 |

(Assume 52 weeks in a year).

Required:

(i) Compute the adjusted partnership profit or loss for the year ended 31 December 2022.

(ii) Distribute the profit or loss to the partners and thus ascertain the taxable income for each partner.

Question 2c

Analyse the Income Tax Act provisions in relation to taxation of collective investment schemes.

Question 3c

The Revenue Authority of your country intends to introduce a tax on digital assets in the next government budget.

During public participation forums, most citizens rejected the proposed digital tax since they were not conversant

with digital assets.

Citing an example, explain what “digital assets” entail.

April 2023

1 Questions

Question 1b

Sema and Tena are partners running a small hardware business in your town. They are facing a tax audit by the

Revenue Authority for failure to maintain complete records. They have approached you to assist them in

ascertaining the taxable profit or loss for the year ended 31 December 2022.

The following information has been provided to you:

| 1. | The partnership deed provides that:

|

| 2. | On 1 September 2022, the partners admitted Vuna and the profit and loss sharing ratio was revised to equal basis for the three partners. Vuna was entitled to interest on capital like the other partners at the rate of 10% per annum. She was not entitiled to any salary or bonus for the year ended 31 December 2022. |

| 3. | Extract of account balances were as follows: | ||

| 31 December 2022 | 31 December 2021 | ||

| Sh. | Sh. | ||

| Accrued bonus due to partners | 1,000,000 | 900,000 | |

| Inventory | 350,000 | 260,000 | |

| Accounts payable | 3,000,000 | 2,600,000 | |

| Prepaid advertising | 210,000 | 440,000 | |

| Outstanding electricity bill | 26,000 | 20,000 | |

| Accounts receivable | 3,900,000 | 2,700,000 | |

| Accrued salaries and wages (excluding partners salaries) | 510,000 | 230,000 | |

| Accumulated depreciation | 700,000 | 440,000 | |

| Capital: Sema | 720,000 | 720,000 | |

| Capital: Tena | 480,000 | 480,000 | |

| Capital: Vuna (Admitted 1 September 2022) | 540,000 | - | |

| 4. | Extracts of cash payments during the year were as follows: | Sh. | |

| Paid to suppliers of goods for resale | 9,000,000 | ||

| Bonus paid to partners shared equally | 1,300,000 | ||

| Cash withdrawn: Sema | 300,000 | ||

| Cash withdrawn: Tena | 350,000 | ||

| Loan interest | 48,000 | ||

| Advertising | 250,000 | ||

| Salaries and wages (including partners salaries) | 4,390,000 | ||

| Motor vehicle expenses | 340,000 | ||

| Electricity | 90,000 | ||

| Computer software | 70,000 | ||

| Purchase of office equipment | 62,000 | ||

| Employee welfare costs | 300,000 | ||

| 5. | Receipts channeled through the bank account were as follows: | Sh. | |

| Proceeds from sale of computers | 55,000 | ||

| Royalty income (net of withholding tax) | 380,000 | ||

| Credit sales | 15,600,000 | ||

| 6. | Cash purchases and cash sales amounted to Sh.900,000 and Sh.2,400,000 respectively and were value added tax (VAT) inclusive. | ||

| 7. | The partners had withdrawn goods for personal use as follows: | Sh. | |

| Sema | 210,000 | ||

| Tena | 70,000 | ||

| No entries were made in the books to record these withdrawals. | |||

| 8. | Hardware goods valued at Sh.60,000 were destroyed in a flood in July 2022. The insurance company agreed to pay Sh.40,000 as compensation but by 31 December 2022, the amount had not been received. |

| 9. | Assume that revenues and expenses accrued evenly throughout the year, unless otherwise specified. |

Required: | |

| (i). | Prepare a statement of taxable profit or loss of the partnership for the year ended 31 December 2022. |

| (ii). | A schedule showing allocation of the profit or loss to the partners for the year ended 31 December 2022. |

December 2022

1 Questions

Question 3a

A, B and C have been trading in a small size partnership sharing profits and losses in the ratio of 2:2:1 respectively.

C retired from the partnership on 31 August 2021 while A and B agreed to continue with the business charging

interest on capital at the rate of 15% per annum as in the previous period when C was still in the partnership.

Due to the changes in the partnership, goodwill was valued at Sh.1,200,000 and was to be written off immediately.

The following trial balance was extracted as at 31 December 2021:

| Sh. | Sh. | |

| Capital account: A | 1,680,000 | |

| Capital account: B | 1,400,000 | |

| Capital account: C | 840,000 | |

| Current account: A | 67,200 | |

| Current account: B | 56,000 | |

| Current account: C | 44,800 | |

| Drawings: A | 78,400 | |

| Drawings: B | 67,200 | |

| Drawings: C | 56,000 | |

| Inventory (1 January 2021) | 252,000 | |

| Purchases and sales | 4,200,000 | 7,720,000 |

| Discount received | 124,000 | |

| Bad debts recovered – general | 193,200 | |

| Salaries and wages | 722,400 | |

| Legal and professional fees | 1,904,000 | |

| Rent & rates | 168,000 | |

| Insurance | 70,000 | |

| Sundry expenses | 50,400 | |

| Trade receivables and payables | 308,000 | 224,000 |

| Allowance for doubtful debts | 11,200 | |

| Land at cost | 2,800,000 | |

| Delivery lorry | 896,000 | |

| Depreciation | 448,000 | |

| Cash at bank | 676,000 | |

| Dividends: Sasa Co-operative Society | 336,000 | |

| 12,696,400 | 12,696,400 |

Additional information:

| 1. | Sales and purchases were inclusive of value added tax (VAT) at the rate of 16%. Cash sales amounted to Sh.358,400 (VAT inclusive) and were excluded from the above accounts. |

| 2. | The following assets were acquired by the business immediately after retirement of C. |

| Sh. | ||

| Computers | 150,000 | |

| Saloon car | 3,120,000 | |

| 3. | Legal and professional fees include: | |

| Sh. | ||

| Stamp duty | 168,000 | |

| Negotiating a bank overdraft | 158,200 | |

| Recovery of bad debts | 245,000 | |

| Signing a 99 year lease agreement | 228,400 | |

| Purchase of A’s private residence | 350,000 | |

| Preparation of employment contract | 82,000 |

| 4. | Interest on drawings was charged at the rate of 10% per annum. |

| 5. | Inventory at year end was valued at Sh.364,000 and the partnership had consistently undervalued inventory at each year end by 20%. |

| 6. | Salary and wages include partners’ salary of Sh.420,000 shared by the partners according to the profit and loss sharing ratio. |

| 7. | Allowance for doubtful debts was to be increased to Sh.24,800 at year end. Bad debts written off amounted to Sh.40,000 of which Sh.8,000 relates to general bad debts. |

| 8. | Prepaid insurance at the beginning of the year amounted to Sh.8,000 while insurance owing at year end amounted to Sh13,000. |

| 9. | Accrued sundry expenses as at 1 January 2021 and 31 December 2021 amounted to Sh.10,000 and Sh.2,000 respectively. |

| 10. | C was paid all his dues on 15 September 2021. The profits and losses were to be shared equally after C’s retirement. |

| 11. | Unless otherwise stated, assume that all revenues and expenses accrued evenly throughout the year. |

Required: | |

| (i). | Prepare a statement of adjusted taxable profit or loss for the partnership for the year ended 31 December 2021. |

| (ii). | Determine the taxable income for each partner. |

August 2022

1 Questions

Question 3c

Explain the tax implications of the following:

(i) Where two or more entities enter into a joint venture agreement or partnership.

(ii) Where shareholders are wholly or partly paid in cash for forfeiting their shares in a cessation of

business.

April 2022

1 Questions

Question 2b

Amua and Beba have carried on business for the last several years under the trade name AB partnership. They share

profits and losses equally with capital contributed earning interest at the rate of 10% per annum.

The following details relate to AB partnership's transactions for the year ended 31 December 2021.

| 1. | Amua and Beba capital accounts reflect credit balances of Sh.1,200,000 for each. |

| 2. | On 1 April 2021, they introduced a new partner Chanda who was to contribute Sh.1,200,000 as his share of capital. They agreed on this day to share profits and losses in the ratio of capital contributed proportional to the period of the year it was invested and that this sharing ratio be backdated to the start ofthe year 2021. |

| 3. | The costs incurred during the year were as follows: | Sh. |

| Salaries and wages for staff | 1,083,000 | |

| Electricity and telephone | 389,000 | |

| Repairs and maintenance | 294,400 | |

| Deprecation and impairments | 420,000 | |

| General insurance | 471,000 | |

| Debenture interest (paid by ABC Ltd.) | 150,360 | |

| Directors fees (including Sh.507,720 partners' salaries) | 1,015,440 | |

| Legal expenses | 510,240 | |

| Medical contributions for partners and directors | 651,840 | |

| Drawings: Amua | 99,000 | |

| Drawings: Beba | 101,400 | |

| Drawings: Chanda | 65,400 | |

| Rent and rates | 315,960 | |

| Motor vehicle running expenses | 500,760 | |

| Printing and stationery | 32,520 |

| 4. | The following assets were purchased during the year: Furniture and fittings Sh.192,000 and a pick-up for Sh.2,160,000. |

| 5. | During the months of the partnership, the total salaries to partners were Sh.507,720. The salaries were to be apportioned according to the period each partner served in the partnership búsiness. |

| 6. | The cost of sales during the year was Sh.21,600,000. Sales were uniform at a margin of 25%. |

| 7. | The partnership was converted into a limited liability company, ABC Ltd. on 1 July 2021 with the partners becoming the new directors of the company. The new firm was listed on the Securities Exchange but not for purpose of raising additional capital. The costs incurred in listing were Sh.100,000. |

| 8. | The sales and expenses accrued evenly throughout the year unless otherwise indicated. |

Required: | |

| (i) | A schedule showing separately the profit or loss for the partnership and the company for the year ended 31 December 2021. |

| (ii) | Tax payable (or refundable) by ABC Ltd. from the profit or loss computed in (b) (i) above. |

| (iii) | A schedule showing the distribution of profits among the partners. |

Pilot December 2021

1 Questions

Question 3b

Mary and Khadija are in a partnership trading as Mahadi enterprises: They share profits and losses in the ratio of 3:2

for Mary and Khadija respectively.

The partners presented the following statement of profit and loss of the partnership for the year ended 31 December

2020.

| Sh. | |

| Sales | 8,400,000 |

| Closing stock | 1,176,000 |

| Rental income | 522,480 |

| Dividend received (net) | 54,240 |

| Foreign exchange gain | 54,960 |

| Interest income (net) | 120,000 |

| Discount received | 84,000 |

| 10,411,680 | |

| Opening stock | 960,000 |

| Purchases | 4,080,000 |

| Salaries and wages | 1,440,000 |

| Insurance | 288,000 |

| Travelling expenses | 187,200 |

| Salaries and wages: Mary | 720,000 |

| Salaries and wages: Khadija | 480,000 |

| Rent rates | 558,000 |

| Interest expense | 1,872,000 |

| Goodwill written off | 120,000 |

| Medical expenses for partners | 240,480 |

| Legal expenses | 144,240 |

| Bank charges | 91,680 |

| Stamp duty | 180,000 |

| Loss on sale of equipment | 19,200 |

| VAT paid | 39,120 |

| Purchase of furniture | 57,600 |

| Depreciation | 48,000 |

| (11,525,520) | |

| Net loss | (1,113,840) |

Additional information:

| 1. | On 1 April 2020 Abby was admitted as a partner. She contributed Sh.960,000 as her share of capital and goodwill. The profit and loss sharing ratio was revised to 2:2:1 for Mary, Khadija and Abby respectively with effect from 1 April 2020. Abby was not entitled to a salary for the year ended 31 December 2020. |

| 2. | Interest expenses comprised: | |

| Sh. | ||

| Interest on capital: Mary | 432,000 | |

| Interest on capital: Khadija | 480,000 | |

| Interest on capital: Abby | 48,000 | |

| Interest on loan | 672,000 | |

| Fridge benefit tax | 240,000 | |

| 1,872,000 |

| 3. | All transactions relating to equipment and furniture occurred after 1 April 2020. |

| 4. | All other revenues and expenses accrued evenly throughout the year. |

Required: | |

| (i) | Determine the adjusted profit or loss of the partnership for the year ended 31 December 2020. |

| (ii) | Allocate the profit or loss computed in (b) (i) above to the partners. |

December 2021

1 Questions

Question 4b

Lipa and Mali are in partnership trading as Lima Enterprises where they share profits and losses in the ratio of 2:1

respectively.

On 1 April 2020, Sasa was admitted with one-third of the profit without altering the existing profit-sharing ratio of Lipa

and Mali.

The following income statement for the year ended 31 December 2020 was provided by the partnership:

| Sh. | Sh. | |

| Gross profit | 2,960,000 | |

| Less: | ||

| Salaries and wages: | ||

| 360,000 | |

| 428,000 | |

| Interest on capital | 150,000 | |

| Current Account: | ||

| 42,000 | |

| 48,000 | |

| Insurance | 24,500 | |

| Motor expenses | 32,500 | |

| Electricity bills | 58,000 | |

| Legal expenses | 142,400 | |

| Audit and accountancy fees | 47,500 | |

| Depreciation | 128,400 | |

| Purchase of furniture | 240,000 | |

| Provision for bad debts | 18,400 | |

| Telephone and postage | 14,200 | |

| General expenses | 354,000 | 2,087,900 |

| Net profit | 872,100 |

Additional information:

1. Insurance represents Mr. Mali's life insurance policy for his family.

2. Interest on capital was prorated and shared according to the profit and loss sharing ratios.

3. Legal expenses included: expenses related to drawing of new partnership deed of Sh.28,000 on admission of

Mr. Sasa, conveyance fees of Sh.14,900 and Sh.36,000 for negotiating a loan facility.

4. General expenses included cost of computers of Sh.90,000 and computer software of Sh.45,000.

5. The firm imported a motor car for use in the partnership business for Sh.800,000. This excluded import duty

of 25% and value added tax at 16%.

Note: Assume that income and expenses accrued evenly during the year.

Required:

(i) Prepare a statement of adjusted taxable profit or loss for the year ended 31 December 2020.

(ii) Total taxable income for each partner.

September 2021

1 Questions

Question 4b

Jirani and Mwema have been partners trading as JM Traders since 1 January 2019. They have not filed individual

income tax returns for the year ended 31 December 2020. The Commissioner for Domestic taxes has issued an

estimated assessment of Sh.940,800 to each of the partners for the year ended 31 December 2020. They share profits

and losses in the ratio of 2:3 to Jirani and Mwema respectively. They are preparing to appeal against the assessment

and have approached you for tax advice with the following details:

| Cashbook summary | |||

| Sh. | Sh. | ||

| Balance brought forward (1 January 2020) | 912,000 | Payment to creditors | 1,056,000 |

| Capital: Jirani | 720,000 | Purchase of furniture | 240,000 |

| Capital: Mwema | 1,080,000 | Motor vehicle expenses | 168,000 |

| Receipts from debtors | 2,040,000 | Electricity expenses | 93,600 |

| Cash sales | 1,200,000 | Rent expenses | 472,800 |

| Rent income | 696,000 | Purchase of motor vehicles | 720,000 |

| Sale of furniture | 204,000 | Salaries and wages | 576,000 |

| Office partitions | 216,000 | ||

| General expenses | 528,000 | ||

| Balance carried forward | 2,781,600 | ||

| 6,852,000 | 6,852,000 | ||

| \(\overline{\underline{\underline{6,852,000}}}\) | \(\overline{\underline{\underline{6,852,000}}}\) | ||

Additional information:

| 1. | Sales and purchases for the year were understated and overstated respectively by 20%. |

| 2. | All the cash sales were paid into the bank with the exception of Sh.528,000 which was debited in the income statement as general expenses but related to the following items:

|

| 3. | The partners are entitled to interest on capital at the rate of 10% per annum on their capital contributions. The interest on capital was included in the figure for purchases for the year. |

| 4. | The cost of furniture sold was Sh.192,000 and had accumulated depreciation of Sh.16,800 as at 1 January 2020. The profit on disposal was credited to the income statements for the year ended 31 December 2020. |

| 5. | Other information provided was as follows: | ||

| 31 December 2019 | 31 December 2020 | ||

| Sh. | Sh. | ||

| Inventories | 297,600 | 434,400 | |

| Creditors for goods | 480,000 | 336,000 | |

| Debtors for goods | 288,000 | 432.000 | |

| Electricity expenses prepaid | 566,400 | 36,000 | |

| Rent owing | 93,600 | 52,800 | |

| Salaries and wages owing | 24,000 | 72,000 | |

| Furniture | 192,000 | 240,000 |

| 6. | The business reported a net loss of Sh.509,400 for the year ended 31 December 2020 after deducting the following expenses:

|

Required:

With supporting computations:

(i) Advise the partners on the accuracy of the estimated assessment issued for the year of income 2020.

(ii) Prepare a schedule of total taxable income for each partner for the year of income 2020.

November 2020

2 Questions

Question 3a

M and K are in partnership trading as MK enterprises. The partners deposited Sh.4,000,000 and Sh.6,000,000 into the business account as their initial capital before commencing trading. They also agreed to share profit and loss in the ratio of their initial capital contribution and interest on capital at 5% per annum on outstanding capital balances.

On 1 January 2018, the firm purchased the following assets for use in the business:

| Sh. | |

| Saloon car | 2,400,000 |

| Computers | 80,000 |

| Furniture and fittings | 96,000 |

| Fax machine | 48,000 |

| Switchboard | 64,000 |

| Bookshelf | 18,000 |

| Office kitchen utensils | 9,000 |

| Office television set | 54,000 |

| Carpets | 36,000 |

| Safe for cash office | 45,000 |

The firm's books were kept in a single entry bookkeeping. The details for the accounting records for the year ended 31 December 2018 obtained were as follows:

| 1 | Sales for the year was Sh. 1,860,000 out of which Sh. 360,000 was on credit and the balance was cash banked. |

| 2 | The following monthly expenses were paid from cash proceeds before banking the proceeds from cash transactions: |

| Sh. | ||

| Transport expenses | 6,000 | |

| Telephone and postage | 5,600 | |

| Office meals | 5,000 | |

| Repairs and maintenance | 4,800 |

| 3 | The bank statements summary for the full year showed payments made during the year as follows: |

| Sh. | ||

| Rent payment | 325,000 | |

| Purchase of 3 tonnes lorry | 1,800,000 | |

| Purchase of motor bike | 90,000 | |

| Office expenses | 1,460,000 | |

| Advertising | 240,000 |

| 4 | The office expenses paid in note (3) above included |

| Sh. | ||

| Partners salaries: M | 270,000 | |

| K | 360,000 | |

| Employees' pension contribution | 420,000 | |

| Donations to society for blind | 78,000 | |

| Tax consultancy fees | 32,000 | |

| Training of partners' children | 28,000 | |

| Motor vehicle insurance | 24,000 |

The business failed to file returns for the year of income 2018 and on 1 July 2019, they received an estimated assessment of Sh.78,000 from the revenue authority for each partner.

Required:

(i). Using the above information, prepare a statement that will form the basis of contesting the estimated assessment for the year of income 2018.

(ii) .Advise the partners on the appeal position.

Question 4b

Anita Warazo has been operating a sole-proprietorship business since 1 January 2015.

The following information was obtained from the books of the business for the past five years.

| Year | 2015 Sh."000" | 2016 Sh."000" | 2017 Sh."000" | 2018 Sh."000" | 2019 Sh."000" |

| Current account balance | 485(Dr) | 600(Cr) | 960(Cr) | 350(Dr) | 560(Cr) |

| Treasury bonds | 1,450 | 940 | 740 | 648 | 780 |

| Pick up (cost) | 900 | 900 | 1,600 | 1,600 | 1,600 |

| Computers (cost) | 150 | 150 | 200 | 200 | 200 |

| Inventory | 170 | 240 | 280 | 376 | |

| Trade receivables | 720 | 600 | 560 | 700 | 840 |

| 10% Mortgage loan | 4,000 | 4,000 | 4,000 | ||

| Trade payables | 460 | 640 | 800 | 560 | 720 |

| Bank loan | 370 | 348 | 400 | 400 | 380 |

| Leasehold property | 1,400 | 1,400 | 1,400 | 1,400 | 1,400 |

| Cash in hand | 560 | 840 | 540 | 600 | 760 |

| Furniture and fittings | 400 | 400 | 300 | 300 | 300 |

| Personal saloon car | - | 480 | 480 | 480 | 480 |

Additional Information:

1. All non-current assets were stated at cost and where the fair value changed was either due to additional met acquired or disposed of.

2. Furniture and fittings whose cost was Sh. 100,000 was disposed of on 1 January 2017 for Sh.68,000.

3. In the year 2016, the proprietor made drawings of Sh.38,000.

4. Anita Warazo paid school fees for her children from business current account of Sh. 138,000 per annum for the years 2016 and 2017.

5. A leasehold property included a property valued at Sh.400,000 inherited from her late father.

6. In the year 2018, she paid insurance premium of Sh.42,000 for her private residence.

7. She contributed to a fundraising in 2019 of Sh.60,000 for supporting a church function.

8. The non-current assets qualified for capital deductions where applicable.

9. Leasehold property comprised a warehouse (cost Sh. 1,000,000) while the inherited property was a dwelling house.

Required:

(i) Prepare a capital statement showing taxable income for the years 2016 to 2019.

(ii) Comment on the tax position of Anita Warazo for each of the years of income

November 2019

1 Questions

Question 1c

Sharon and Primus are partners running a hardware business. They have approached you to assist them prepare the

partnership returns for the year ended 31 December 2018. The following information has been presented to you:

Hint: Ignore opening and closing inventory.

| 1 | The partnership agreement provides that:

|

| 2 | The balances in the books of account as at 31 December 2018 and 31 December 2017 included the following: |

| 31 December 2018 Sh. | 31 December 2017 Sh. | ||

| Accrued commission due to partners | 400,000 | 360,000 | |

| Accounts payable (trade) | 2,000,000 | 1,600,000 | |

| Accrued advertising expense | 610,000 | 340,000 | |

| Prepaid royalty income | 160,000 | 100,000 | |

| Accounts receivable (trade) | 5,900,000 | 1,700,000 | |

| Accrued salaries and wages (partners excluded) | 410,000 | 130,000 | |

| Accumulated depreciation | 600,000 | 340,000 | |

| 3 | Extracts of cash payments during the year were as follows: | ||

| Sh. | |||

| Commission paid to partners equally | 100,000 | ||

| Purchases (goods for sale) | 1,000,000 | ||

| Advertising expenses | 150,000 | ||

| Salaries and wages (partners excluded) | 1,390,000 | ||

| Motor vehicle expenses | 240,000 | ||

| Electricity expenses | 80,000 | ||

| Office partitions | 60,000 | ||

| Purchase of office equipment | 97,000 | ||

| Meals to employees | 200,000 | ||

| Loan interest | 35,000 | ||

| Cash withdrawn by partners - Sharon | 160,000 | ||

| - Primus | 100,000 | ||

| 4 | All receipts were channeled through the account and included the following: | ||

| Sh. | |||

| Sales (all were on credit terms) | 1,600,000 | ||

| Royalty income | 240,000 | ||

| Proceeds from sale of office equipment | 45,000 | ||

| Computer leasing charges | 6,000 | ||

| 5 | The partners withdrew hardware goods for personal use as indicated below: | ||

| Sh. | |||

| Sharon | 110,000 | ||

| Primus | 60,000 | ||

| 6 | In December 2018, some of the hardware goods which were valued at Sh.60,000 were destroyed by fire... Compensation of Sh.35,000 was received from the insurance company. |

Required: | |

| (i) | Taxable profit or loss of the partnership for the year ended 31 December 2018. |

| (ii) | A schedule showing the partners allocation of taxable income or loss. |

May 2019

2 Questions

Question 4b

Solomon Omariba started a merchandise business, Solo Traders, on I January 2016. He had not filed individual

income tax returns for the years of income 2016 and 2017. The revenue authority announced a tax amnesty, where one

qualified provided they filed returns for the year of income 2018.

Mr Omariba has provided the following details to you to assist in filing his returns:

| 1 | An analysis of the cash book for the year ended 31 December 2018 is as shown below: |

| Cash book - Bank Column | ||||

| Sh. | Sh. | |||

| 1 January 2018 balance brought down | 970,000 | Fixtures and fittings (acquisition) | 183,000 | |

| Cash sales | 4,408,000 | Suppliers of goods | 696,000 | |

| Cheques from customers | 649,600 | Bank charges | 14,800 | |

| Refunds from suppliers | 41,760 | Motor vehicle (acquisition) | 500,000 | |

| Rent income | 520,000 | Salaries and wages | 480,000 | |

| Sale of fixtures | 248,000 | Office computers (acquisition) | 240,000 | |

| Rent and rates | 62,000 | |||

| Electricity expenses | 58,000 | |||

| Telephone and postage | 62,640 | |||

| Refunds to customers | 37,120 | |||

| Computer software | 60,000 | |||

| Balance carried down | 4,443,800 | |||

| 6,837,360 | 6,837,360 | |||

| 2 | Other information obtained from the books of account included: |

| 1 January 2018 | 31 December 2018 | ||

| Inventory | 4,320,000 | 225,000 | |

| Suppliers of goods | 278,400 | 139,200 | |

| Trade debtors | 174,000 | 487,200 | |

| Accrued electricity | 66,120 | 113,680 | |

| Prepaid rent income | 180,000 | 240,000 | |

| Motor vehicles | 1,400,000 | 1,800,000 | |

| Prepaid salaries and wages | 320,000 | 140,000 | |

| Fixtures and fittings | 450,000 | 170,000 |

| 3 | Non-current assets are stated at cost. However, the business had charged depreciation in the income statement. |

| 4 | Opening and closing inventories were overvalued and undervalued by 20% and 10% respectively. |

| 5 | All operating expenses and non-current assets comprise 40% non-business activities. |

| 6 | Total sales and purchases are inclusive of value added tax at the rate of 16%. |

| 7 | The business had issued credit notes of Sh.34,800 for goods returned by credit customers. |

| 8 | The cost of fixtures disposed of was Sh.220,000. |

| 9 | From the accounting records, the accountant had reported a net loss of Sh.186,400. |

Required:

A statement showing the corrected adjusted taxable income of Solo Traders for the year of income 2018.

Question 5b

The following are the year 2018 records of the Trustees of the late Kalume Tajiri Children Settlement created in

favour of his three children; Baraka, Khalifi and Mwanga.

Required:

| Sh."000" | |

| Gross rental income | 800,000 |

| Trading income | 310,000 |

| Dividends (gross) | 160,000 |

| Sundry income | 90,000 |

Additional information:

| 1 | Each beneficiary is entitled to 1/5 share of the net distributable income. |

| 2 | Interest on debt repayment by the settlement is Sh.14,000,000. |

| 3 | Fixed annuity to beneficiary is Sh.120,000,000 (gross). |

| 4 | Trustees remuneration per "Trust Deed":

|

| 5 | Under the terms of the Trust Deed, the trustees made the following discretionary payments to Baraka, Khalifi and Mwanga; Sh.120,000,000, Sh.100,000,000 and Sh.60,000,000 respectively. |

| 6 | Trading income was before taking into account capital expenditure as follows: |

| Sh. | ||

| Godown | 3,500,000 | |

| Staff canteen | 750,000 | |

| Parking bay | 800,000 | |

| Sports pavilion | 1,950,000 | |

| 7,000,000 |

| 7 | Administrative and other expenses amounted to Sh.160,000,000. |

| 8 | The children did not have other income. |

Required:

(i) A statement of income tax payable by the trustees on the trust income for the year of assessment 2018.

(ii) The amount due to each beneficiary for the year of assessment 2018.

May 2018

1 Questions

Question 3a

Jua and Kali have been trading as partners under a trade name Juakali Enterprises since 1 January 2016. They have

not filed individual income tax returns for the year ended 31 December 2017. The Commissioner of Domestic Taxes

has issued an estimated assessment of Sh.784,000 to each of the partners for the year ended 31 December 2017. They

share profits and losses in the ratio of 2:3 to Jua and Kali respectively. They are preparing to appeal against the

assessment and have approached you for tax advice with the following details:

Required:

| Cash book summary | |||

| Dr. | Sh. | Cr. | Sh. |

| Balance brought forward (1 January 2017) | 760,000 | Payments to creditors | 880,000 |

| Capital: Jua | 600,000 | Purchase of furniture | 200,000 |

| Kali | 900,000 | Motor vehicle expenses | 140,000 |

| Receipts from debtors | 1,700,000 | Electricity expenses | 78,000 |

| Cash sales | 1,000,000 | Rent expenses | 394,000 |

| Rent income | 580,000 | Purchase of motor vehicle | 600,000 |

| Sale of furniture | 170,000 | Salaries and wages | 480,000 |

| Office partitions | 180,000 | ||

| General expenses | 440,000 | ||

| Balance carried forward | 2,318,000 | ||

| 5,710,000 | 5,710,000 | ||

Additional information:

| 1 | The cost of furniture sold was Sh.160,000 and had accumulated depreciation of Sh.14,000 as at 1 January 2017. Profit on disposal was credited to the income statement for the year ended 31 December 2017. |

| 2 | All the cash sales were paid into the bank with the exception of Sh.440,000 which was debited in the income statement as general expenses, but related to the following items: partners' children school fees, Sh.80,000, purchase of goods Sh.200,000, tax appeal expenses Sh.40,000, insurance policy for partners' life Sh.70,000 and computer software Sh.50,000. |

| 3 | Other information provided was as follows: |

| 31 December 2016 Sh. | 31 December 2017 Sh. | ||

| Inventories | 248,000 | 362,000 | |

| Creditors for goods | 400,000 | 280,000 | |

| Debtors for goods | 240,000 | 360,000 | |

| Electricity expenses prepaid | 472,000 | 30,000 | |

| Rent owing | 78,000 | 44,000 | |

| Salaries and wages owing | 20,000 | 60,000 | |

| Furniture | 160,000 | 200,000 |

| 4 | The business reported a net loss of Sh.424,500 for the year after deducting the following expenses:

|

| 5 | Sales and purchases for the year were understated and overstated respectively by 20%. |

| 6 | The partners are entitled to interest on capital at the rate of 10% per annum on their capital contributions. The interest on capital was included in the figure for purchases for the year. |

Required:

(i) With supporting computations, advise the partners on the accuracy of the estimated assessment issued for the

year of income 2017.

(ii) Prepare a schedule of total taxable income for each partner for the year of income 2017. (5 marks)

Hint: Start with the adjusted net loss.

November 2017

1 Questions

Question 2a

Masai Traders commenced trading on 1 January 2014. The following are the financial statements and supporting

records for the years ended 31 December 2016 and 2015:

Required:

Statement of comprehensive income for the year ended 31 December 2016:

| Sh. "000" | Sh. "000" | |

| Sales | 82,600 | |

| Less cost of goods sold | (36,200) | |

| Gross profit | 46,400 | |

| Less expenses: | ||

| Legal expenses | 7,700 | |

| Impairment loss on business premises | 4,800 | |

| Depreciation on plant and equipment | 1,600 | |

| Interest expense | 478 | |

| Salaries and wages | 1,394 | (15,972) |

| Net profit | 30,428 | |

Statement of financial position as at 31 December: | ||

| 2016 Sh. "000" | 2015 Sh. "000" | |

| Non-current assets: | ||

| Business premises | 3,200 | 3,500 |

| Plant and equipment | 26,400 | 28,000 |

| Saloon car | 800 | 860 |

| 30,400 | 32,360 | |

| Current assets: | ||

| Inventories | 11,600 | 11,200 |

| Debtors | 12,800 | 15,200 |

| Cash and cash equivalents | 14,200 | 8,600 |

| 69,000 | 67,360 | |

| Financed by: | ||

| Capital | 30,000 | 30,000 |

| Add: net profit | 30,428 | 24,240 |

| 60,428 | 54,240 | |

| Current liabilities: | ||

| Creditors | 4,572 | 3,120 |

| Bank overdraft | 4,000 | 10,000 |

| 69,000 | 67,3.60 | |

Additional information:

| 1 | During the year 2016, payments through the bank comprised the following: |

| Sh."000" | ||

| Conveyance fees for business land title deed | 128 | |

| Payments to creditors | 2,488 | |

| Salary to wife | 260 | |

| Mortgage interest; personal residence | 184 | |

| Defending business against illegal trade | 160 | |

| Revenue stamps | 16 |

| 2 | The credit purchases figure was overstated by 60%. |

| 3 | Receipts from debtors amounted to Sh.9,600,000. A debtor owing goods valued at Sh.85,840 inclusive of 16% VAT was declared bankrupt during the year and the debt written off. The write off was included in the interest expense. |

| 4 | The figure for sales was understated by 20%. |

| 5 | Business premises included:

|

| 6 | There were no acquisitions or disposals of fixed assets during the year 2016. |

| 7 | Plant and equipment acquired in the year 2015 includes:

|

Required:

(i) A statement of adjusted taxable profit or loss for the year ended 31 December 2016.

(ii) State three areas or items that you might require further clarification on from Masai Traders for accurate

computation of any tax due.

May 2017

2 Questions

Question 3b

Wema and Nenda have been running Wenda Enterprises as a partnership, sharing profits and losses in the ratio of 2:3

respectively. The following is the statement of comprehensive income for the firm for the year ended 31 December

2016:

Required:

| Sh. | Sh. | |

| Sales | 5,220,000 | |

| Less: Cost of goods sold | (2.047,000) | |

| Gross profit | 3,173.000 | |

| Rental income | 148,800 | |

| Foreign exchange gain | 120,200 | |

| İnterest on fixed deposit account | 80,000 | |

| 3,522,000 | ||

| Less: Expenses | ||

| Purchase of CCTV cameras | 96,000 | |

| Impairment loss on godown | 124,600 | |

| Website development | 130,000 | |

| Debenture interest | 56,000 | |

| Audit fees | 48,400 | |

| Salaries and wages | 300,000 | |

| Directors' allowances | 280,000 | |

| Legal expenses | 250,000 | |

| Loss on rented property | 36,200 | |

| Purchase of foreign currency | 344,900 | |

| Advertising expenses | 224,200 | |

| Purchase of computers | 180,000 | |

| Insurance | 94,200 | |

| Medical expenses | 49,600 | |

| Bank charges | 82,400 | |

| Purchase and installation of computer programs | 120,000 | (2,416,500) |

| 1,105,500 |

| 1 | The business was converted into a limited liability company trading as Dawadu Ltd. with effect from 1 October 2016 and retaining the partners as directors of the new company. |

| 2 | The cost of goods sold included opening stock of Sh.576,000 which was overcast by 20%, purchases of Sh.2, 146,000 inclusive of 16% VAT and closing stock of Sh.675,000 which was undercast by 10%. |

| 3 | All revenues and expenses accrued evenly throughout the year except for specific expenses relating to Dawadu Ltd. as a company. |

| 4 | Salaries and wages included partners' salaries of Sh.120,000. |

| 5 | Legal expenses comprised: | Sh. |

| Acquisition of company's title deed | 50,000 | |

| Negotiating debenture stock | 100,000 | |

| Demand letters to customers | 40,000 | |

| Drafting Memorandum of Association | 60,000 | |

| 250,000 |

| 6 | Wema was paid consultancy fees of Sh.54,000 for installing CCTV cameras in the premises. |

| 7 | Advertising expenses include a neon sign costing Sh.92,000. |

| 8 | The sales figure was inclusive of VAT at the rate of 16% |

| 9 | Directors' allowances include commission paid to Nenda of Sh.60,000 for negotiating a business contract. |

Required:

(i) Separate statements of adjusted taxable profit or loss for Wenda Enterprises and Dawadu Ltd. for the year

ended 31 December 2016. (Hint: Start with the net profit).

(ii) Tax payable by (or refundable to) Dawadu Ltd. for the year ended 31 December 2016.

Question 5b

A and B are partners trading as AB Enterprises. sharing profits and losses equally.

The following is the statement of comprehensive income for the partnership for the year ended 31 December 2016:

| Sh."000" | Sh."000" | |

| Sales | 40,450 | |

| Less: Sales returns | (1,200) | |

| 39,250 | ||

| Less: Cost of goods sold | (19,550) | |

| Gross profit | 19.700 | |

| Discount received | 350 | |

| 20,050 | ||

| Less: Expenses | ||

| Rent | 1,850 | |

| Bad debts | 400 | |

| Wages and salaries | 6,100 | |

| Loan interest | 400 | |

| Depreciation | 4,200 | |

| Insurance | 1,450 | |

| Repairs | 300 | |

| Electricity | 750 | (15,450) |

| Net profit | 4,600 |

The partnership is under tax investigation and the assessor obtained the following details from the firm's records for

the year ended 31 December 2016:

| 1 | Balances of assets and liabilities: | 1 January 2016 Sh."000" | 31 December 2016 Sh."000" |

| Inventory | 6,100 | 4,200 | |

| Machinery | 84,600 | 97.000 | |

| Rent prepaid | 800 | - | |

| Rent owing | - | 950 | |

| Debtors | 9,300 | 7,500 | |

| Loan from bank at 8% interest per annum | 6,000 | 6,000 | |

| Loan interest owing | - | 200 | |

2 | Receipts and payments were as follows: | ||

| Sh."000" | |||

| Receipts: | |||

| Receipts from debtors | 26,400 | ||

| Cash sales | 72,400 | ||

| Payments: | |||

| Loan interest paid | 400 | ||

| Electricity | 750 | ||

| Rent | 240 | ||

| Purchase of machinery | 16,400 |

| 3 | Rent expense related to A's private residence. In addition, electricity paid includes Sh.50,000 for A's private residence. |

| 4 | The tirm issued credit notes amounting to Sh. 1,200,000 which was erroneously posted as Sh.200,000 to the relevant ledgers. |

| 5 | Included in the sales figure is Sh.30,000 for interest on drawings by B and proceeds on disposal of machinery Sh.1,450,000. The machinery had cost Sh.4,000,000 with an accumulated depreciation of Sh.200,000. |

| 6 | Receipts from debtors include Sh.440,000 contributed by a new partner C as his capital on 1 October 2016.The profit and loss sharing ratio changed te 2:2:1 for A, B and C respectively. |

| 7 | Purchases amounted to Sh.19,250,000 which included goods withdrawn by B valued at Sh.300,000. |

| 8 | Salaries and wages include accrued salaries to the partners of Sh.2,400,000 shared equally among all the three partners per month as applicable. |

Required:

As a tax assessor, compute the net profit for tax purposes for the year ended 31 December 2016 indicating the taxable

income for each partner.

November 2016

2 Questions

Question 1b

Ali and Baba are partners in a small firm trading as Alibaba Enterprises. They share profits and losses in the ratio of

2:3 respectively.

The following extracts were obtained from the records of the firm for the year ended 31 December 2015:

| 1 | Partners' current account extracts: |

| Debit | Credit | |||||

| Ali Sh. | Baba Sh. | Ali Sh. | Baba Sh. | |||

| Drawings | 40,000 | 60,000 | Balance brought down | 100,000 | 200,000 | |

| Salaries to partners | 70,000 | 120,000 | ||||

| Interest on capital | 50,000 | 40,000 |

| 2 | Assets and liabilities: | ||

| 1 January 2015 Sh. | 31 December 2015 Sh. | ||

| Saloon car (cost) | 2,400,000 | 2,160,000 | |

| Trade receivables | 1,800,000 | 960,000 | |

| Donations | - | 140,000 | |

| Salaries and wages accrued | 840,000 | 1,600,000 | |

| Electricity prepaid | 170,000 | 200,000 | |

| Furniture | 200,000 | 180,000 | |

| Inventories | 360,000 | 500,000 | |

| Trade payables | 1,500,000 | 1,200,000 |

| 3 | Extracts from the bank statement: | |

| Sh. | ||

| Payments to suppliers for goods | 840,000 | |

| Receipts from customers | 2,200,000 | |

| Payments for computers (hardware) | 600,000 | |

| Payments for computer software | 120,000 | |

| Catering fees | 90,000 | |

| Electricity | 60,000 | |

| Salaries and wages | 700,000 | |

| Legal fees | 160,000 |

| 4 | Legal fees amounting to Sh.48,000 relate to costs of negotiating purchase of business premises while electricity paid included a deposit of Sh. 15,000 to the power company. |

| 5 | Each partner had obtained a 10% loan of Sh.200,000 from the partnership for acquiring their private assets. The interest on loan was included in their share of interest on capital. |

Required:

(i) A statement of adjusted taxable profit or loss of the partnership for the year ended 31 December 2015.

(ii) Total taxable income (loss) for each partner.

Question 2b

The following information was extracted from the books of Michezo Sporting Members Club for the year ended 31 December 2015. The club's manager did not submit income tax returns as he argued that the club was exempted from taxation. He has consulted you for professional advice.

Additional information:

| 1 | The club received gross income during the year ended 31 December 2015 amounting to Sh.35 million which was analysed as follows: |

| Sh. | ||

| Entrance fees | 4,770,000 | |

| Member subscription | 15,900,000 | |

| Interest on late subscription | 795,000 | |

| Interst income (fixed deposit) | 2,544,000 | |

| Dividend income | 1,272,000 | |

| Royalties | 1,908,000 | |

| Rent income | 6,360,000 | |

| Gain on property transfers | 1,451,000 | |

| 35,000,000 |

| 2 | Operating expenses amounted to Sh.6,360,000 |

| 3 | Interest and dividend income were stated gross of tax. |

Required:

(i). Advise the club's manager on the circumstances under which members clubs are taxed in your country.

(ii). Assess whether Michezo Sporting Members Club is subject to taxation for the year ended 31 December 2015 and the applicable tax liability (if any).

May 2016

1 Questions

Question 2

Weka Enterprises is a small retail business dealing in fast moving consumer products The Revenue Authority suspects that the business has been filing fraudulent returns and bas requested for financial statements from the business. The business provided the following derails for the years ended 31 December 2015 and 31 December 2014

| Income statement for the year ended 31 December 2015 | ||

| Sh. | Sh. | |

| Turnover | 27,840,000 | |

| Less cost of goods sold | (15,354,000) | |

| Gross profit | 12,486,000 | |

| Proceeds from sale of furniture | 240,000 | |

| Capital gain on sale of plot | 156,400 | |

| 12,882,400 | ||

| Less expenses | ||

| Purchase of furniture | 360,000 | |

| General expenses | 2,367,800 | |

| Rent and rates | 160,000 | |

| Depreciation on motor vehicle | 94,600 | |

| Customs duty | 124,200 | |

| Hire purchase cost | 226,000 | |

| Salaries and wages | 1,680,000 | (5,012,600) |

| Net profit | 7,869,800 | |

| Statement of financial position as at 31 December 2015 | ||

Non-current assets | 2015 Sh. | 2016 Sh. |

| Furniture at cost | 348,000 | 460,000 |

| Motor vehicle at cost | 1,660,000 | 1,565,400 |

| 2,008,000 | 2,025,400 | |

| Current assets | ||

| Inventories | 4,389,600 | 2,881,000 |

| Accounts receivable | 740,400 | 1,640,000 |

| Prepaid general expenses | 178,200 | 98,000 |

| Prepaid rent and rates | 72,800 | 24,600 |

| Cash and cash equivalent | 300,000 | 183,000 |

| Total assets | 7,689,000 | 6,852,000 |

| Financed by: | ||

| Capital | 1,000,000 | 800,000 |

| Add net profit | 7,869,800 | 5,780,000 |

| 8,869,800 | 6,580,000 | |

| Less drawings | (2,200,000) | (1,320,000) |

| 6,669,800 | 5,260,000 | |

| Current liabilities | ||

| Accounts payable | 979,200 | 1,528,000 |

| Accrued rents and rstes | 24,000 | 36,000 |

| Interest due on higher purchase | 16,000 | 28,000 |

| Total capital and liabilities | 7,689,000 | 6,852,000 |

Additional information:

| 1 | Turnover and purchases were inclusive of VAT at the rate of 16%. |

| 2 | The turnover excludes cash sales. During the year ended 31 December 2015, the business paid the following expenses out of cash sales. |

| Sh. | ||

| Telephone and postage | 48,000 | |

| School fees | 142,800 | |

| Repairs and maintenance | 94,600 | |

| Insurance | 36,600 |

| 3 | The bank balance is included in the cash and cash equivalents. The following details were included in the bank statement: |

| Sh. | ||

| Personal expenses | 294,000 | |

| General expenses | 792,800 | |

| Rent and rates | 68,400 | |

| Hire purchase interest | 29,600 | |

| Payments to creditors | 2,460.000 | |

| Receipts from debtors | 5,890,000 |

| 4 | The following assets used by the business were not included in the assets register. Sh |

| Computers | 368,000 | |

| Fax machine | 120,000 | |

| Salon car | 2,800,000 | |

| Delivery van | 720,000 | |

| Computer software | 150,000 |

The revenue authority has established that the statement of financial position forms a good basis for recomputing the taxable profit. All expenses are to be adjusted on the basis of the statement of financial position.

Required:

(a) Using suitable computations, confirm the accuracy or otherwise of the taxable profit of enterprises for the year ended 31 December 2015

(b) Summarise five types of preliminary information that you might require from the business in order to further ascertain the accuracy of the taxable profit

November 2015

1 Questions

Question 3

James and Katana established a partnership business, sharing profits and losses in the ratio of 3:2 respectively. The following is

the income statement of the partnership for the year ended 31 December 2014:

| Sh. | Sh. | |

| Sales | 6,728,000 | |

| Unrealised foreign exchange gain | 150,000 | |

| Capital gain on sale of shares | 352,000 | |

| Recovery from insurance on stock stolen | 480,000 | |

| Goods transferred to a branch at cost | 184,000 | |

| Dividends from Kali Cooperative Society | 51,000 | |

| 7,945,000 | ||

| Less expenses: | ||

| Purchases | 2,842,000 | |

| Purchase of computers | 180,000 | |

| Partners salaries | 720,000 | |

| Legal fees | 680,000 | |

| Repairs and maintenance | 568,400 | |

| Rent and rates | 244,600 | |

| Interest on loan | 166,200 | |

| General expenses | 964,000 | |

| Motor vehicle expenses | 840,000 | |

| Insurance | 156,000 | |

| Preliminary expenses | 262,800 | |

| Directors fees | 600,000 | |

| Audit fees | 148,200 | |

| Debenture interest | 360,000 | |

| Travelling expenses | 960,000 | 8,828,200 |

| Net loss | (883,200) |

Additional information:

| 1 | The partnership was converted into a limited liability company by the name Kaka Ltd. on 1 October 2014. Incomes and expenses accrued evenly throughout the year unless otherwise stated. |

| 2 | Purchases and sales were inclusive of value added tax at a rate of 16%. |

| 3 | Closing stock was valued at Sh.1,840,000 while opening stock was at 10% of sales net of value added tax. |

| 4 | Legal fees comprised: | Sh. |

| Petition to Association of Manufacturers | 80,000 | |

| Notice for change of business name | 64,800 | |

| Conveyance fees of business | 72,400 | |

| Premises Stamp duty | 36,600 | |

| Negotiating a business loan | 20,800 | |

| Recovery of bad debts | 45,000 | |

| Signing a 100-year lease agreement | 128,400 | |

| Purchase of partner's private residence - James | 150,000 | |

| Appeal against tax arrears | 82,000 | |

| 680,000 | ||

| 5 | Repairs and maintenance comprised: | Sh. |

| Purchases of furniture | 96,000 | |

| Installation of neon sign | 60,000 | |

| Designing an office block | 140,000 | |

| Cost of partitioning office block | 250,000 | |

| Repainting of business premises | 22,400 | |

| 568,400 |

| 6 | General expenses included; registering of patent rights Sh.64,000, floatation costs Sh.48,000 and negotiating costs for an additional piece of land for business expansion at Sh.56,000. |

| 7 | Interest on loan includes interest on partners' capital of Sh.100,000 which was shared according to profit and loss sharing ratio. |

Required:

(a) A statement of adjusted taxable profit or loss for the business for the year ended 31 December 2014.

Hint: Start with gross profit.

(b) Comment on the tax position of James, Katana and the company.

(c) Citing examples, advise James and Katana on two areas of tax avoidance that they could explore for the business.

May 2015

1 Questions

Question 5b

Kimutai and Wakoli started an accountancy firm on 1 January 2014 under the name Kimutai Wakoli and Associates. They deposited Sh. 3,000,000 and Sh. 2,000,000 as capital respectively and agreed that the profits and losses would be shared equally They also agreed that interest on capital would be paid at the rate of 5% per annum based on the initial capital contributions.

The firm did not maintain the necessary books of account, but provided the following additional information

Required:

Taxable profit (or loss) for the partnership for the year ended 31 December 2014

The firm did not maintain the necessary books of account, but provided the following additional information

| 1 | On 5 January 2014, the firm signed a six year lease for an office at an annual lease payment of Sh. 200,000. A deposit equivalent to two years lease was paid on commencement of the lease |