CPA Advanced Taxation – August 2023 Past Paper & Answers

Unit: Advanced Taxation

15 Questions

Join the community! 550+ students upgraded in the last 24 hours.

Limited Discount Seats Available

Questions

Download CPA Advanced Taxation August 2023 past paper with detailed answers and marking scheme. This paper is based on KASNEB examination standards and is ideal for revision and exam preparation.

Access the full paper online, download the PDF, or study offline. Each question includes step-by-step solutions to help you understand key concepts in Advanced Taxation.

1a

Professional practice in taxation

Tax systems and policies

Discuss how the following issues may generate ethical dilemmas to a tax professional:

(i) Conflict of interest.

(ii) Contingent fee tax representations.

1b

Tax systems and policies

Describe THREE criteria for evaluating modern tax systems.

1c

Tax investigations

Professional practice in taxation

Summarise FOUR signs that may point to tax fraud in a business entity.

1d

Taxation of cross border activities

Tax planning

Tax systems and policies

Citing FOUR reasons, argue the case for double taxation agreements as tax incentives.

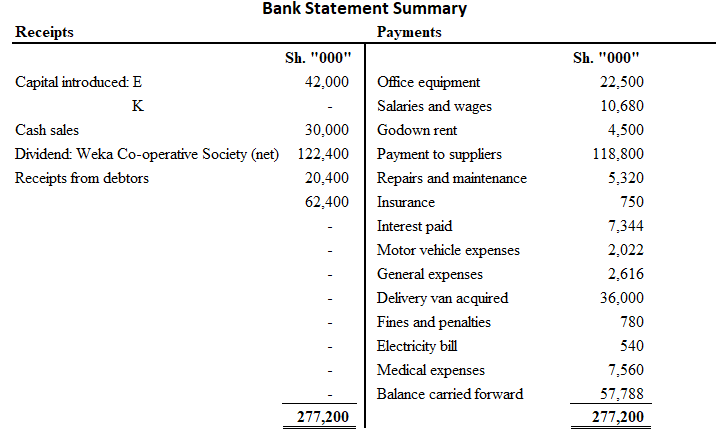

2a

Taxation of business income and specialized business activities

E and K commenced trading as partners under the name EK Enterprises on 1 January 2022. They share profits and

losses equally and were entitled to receive monthly salaries of Sh.240,000 and Sh.288,000 for E and K respectively.

The partnership did not maintain a complete set of accounting records. The following is a summary of the partnership’s

bank statement for the year ended 31 December 2022:

Additional information:

| 1. | As at 31 December 2022, the partnership owed suppliers Sh.9,360,000 while the amount owed by customers was Sh.10,740,000. |

| 2. | Rebate received from suppliers amounted to Sh.1,590,000 and discount allowed to customers amounted to Sh.1,416,000. |

| 3. | Bad debts amounted to Sh.984,000 out of which Sh.240,000 relate to a loan advanced to E that was overdue. |

| 4. | Closing stock was valued at Sh.7,440,000 as at 31 December 2022. |

| 5. | Salaries and wages include salary to the partners for the year. |

| 6. | Included in the interest expense is interest on partners’ capital contribution at the rate of 8% per annum. |

| 7. | The annual rent for the godown was Sh.5,400,000. |

| 8. | As at 31 December 2022, electricity and insurance owing amounted to Sh.300,000 and Sh.153,600 respectively. |

| 9. | The following payments were made in cash from cash sales before banking: |

| 9. | Sh. | |

| Motor vehicle expenses (per annum) | 1,656,000 | |

| Wages (per annum) | 1,944,000 | |

| Sundry expenses (per annum) | 420,000 | |

| Weekly drawings: E | 86,400 | |

| Weekly drawings: K | 46,800 |

(Assume 52 weeks in a year).

Required:

(i) Compute the adjusted partnership profit or loss for the year ended 31 December 2022.

(ii) Distribute the profit or loss to the partners and thus ascertain the taxable income for each partner.

2b

Tax dispute resolution mechanism

Professional practice in taxation

Alternative Dispute Resolution (ADR) methods are utilised by revenue authorities to resolve and expedite tax related

disputes on a timely basis. While ADR mechanisms present many advantages, they also face certain challenges when

applied to tax matters.

Explain SIX challenges faced in the administration of ADR in your country.

2c

Taxation of business income and specialized business activities

Tax systems and policies

Analyse the Income Tax Act provisions in relation to taxation of collective investment schemes.

3a

Taxation of cross border activities

Professional practice in taxation

Evaluate FOUR methods that multinational companies operating in Kenya can use in order to adjust transfer prices

for purposes of computing taxable income as provided under the Transfer Pricing Rules (2006).

3b

Limited companies

Tax investigations

Nalo Ltd. started a small merchandise business on 1 January 2022. The company did not maintain a set of complete

records and as such has not filed income tax returns for the year of income 2022. The Revenue Authority has sent

the company a demand notice of Sh.2,200,000 as the tax due for the year 2022.

The company director has approached you and requested that you assist in ascertaining the correct tax liability and

also advise him on whether to object the demand notice.

The following details have been availed:

| 1. | Analysis of the bank account for the year ended 31 December 2022 revealed the following: | |||

| DR | CR | |||

| Sh. | Sh. | |||

| Balance brought forward 1 January 2022 | 1,940,000 | Fixtures and fittings (cost) | 366,000 | |

| Cheques from customers | 1,299,200 | Suppliers of goods | 1,392,000 | |

| Refund from suppliers | 83,530 | Bank charges | 29,600 | |

| Rental income | 1,040,000 | Delivery van at cost | 1,000,000 | |

| Sale of fixtures | 96,000 | Salaries and wages | 1,060,000 | |

| Cash sales | 8,816,000 | Computers at cost | 480,000 | |

| - | - | Rent and rates | 124,000 | |

| - | - | Electricity | 116,000 | |

| - | - | Telephone and postage | 125,800 | |

| - | - | Refunds to customers | 74,250 | |

| - | - | Computer software cost | 120,000 | |

| - | - | Balance carried forward | 8,387,090 | |

| - | 13,274,730 | - | 13,274,730 | |

| 2. | Other information obtained from the books of accounts included: | ||

| 1 January 2022 Sh. | 1 December 2022 Sh. | ||

| Inventory | 4,320,000 | 2,250,000 | |

| Suppliers of goods | 478,200 | 239,200 | |

| Trade debtors | 348,000 | 960,000 | |

| Accrued electricity | 66,000 | 116,000 | |

| Lorry | 1,400,000 | 1,400,000 | |

| Prepaid wages and salaries | 320,000 | 140,000 | |

| Rent and rates owing | 45,000 | 17,000 | |

| 3. | All non-current assets were acquired in the course of the year. The cost of fixtures sold was Sh.220,000. |

| 4. | Opening and closing inventories were undervalued and overvalued by 20% and 10% respectively. |

| 5. | Cash purchases amounted to Sh.2,400,000. All sales and purchases are inclusive of value added tax (VAT) at the rate of 16%. |

| 6. | The business issued credit notes of Sh.34,800 for goods returned by credit customers and received discount from suppliers of Sh.52,000. |

Required: | |

| (i) | Prepare a statement showing the correct adjusted taxable income and tax payable (if any) for the year ended 31 December 2022. |

| (ii) | Advise the director on the action to take on the demand notice. |

3c

Taxation of business income and specialized business activities

Tax systems and policies

The Revenue Authority of your country intends to introduce a tax on digital assets in the next government budget.

During public participation forums, most citizens rejected the proposed digital tax since they were not conversant

with digital assets.

Citing an example, explain what “digital assets” entail.

4a

Tax systems and policies

Professional practice in taxation

Assume that your country has continued to face challenges in addressing tax deficits. Over the past few years, the

revenue from taxation has not fully met the country’s development needs.

Required:

As a tax expert, advise the revenue authority in your country on FIVE possible reasons for the shortfall in tax

collection.

4b

Taxation of business income and specialized business activities

Limited companies

Value added tax administration

Tax systems and policies

KK Realtors are in the real estate business. They rent out two prime highrise buildings, one a residential apartment

and the other an office block. They are registered for the monthly residential rental obligation as well as filing for

value added tax (VAT).

Details of their transactions for the month of December 2022 are provided below:

| Incomes | Sh.“000” |

| Rent: Apartment | 1,248,450 |

| Rent: Office block | 7,244,200 |

| Expenses: | |

| Garbage collection | 75,864 |

| Sewerage | 92,8090 |

| Repairs and maintenance (outsourced to local company) | 144,420 |

| Housing agents fee (5% of income) | ? |

| Security firm (eight day and eight night guards) | 464,000 |

| Insurance | 580,000 |

| Interest on bank loan | 139,200 |

| Caretakers’ salaries | 92,800 |

| Webhosting (by South Africa-based company) | 67,280 |

| Audit and assurance fee | 1,334,000 |

| Telephone and electricity | 52,952 |

| Other staff salaries | 992,496 |

| Architect’s fee (based in France) | 184,730 |

The following additional information is provided:

1. With the exception of housing agents fee, webhosting and architect’s fee, a quarter of the expenses relate

to the residential business while the rest relate to the office block.

2. Housing agents fee accrues based on the amount paid for income collected from each property.

3. Webhosting and architects fee could not be directly attributed to either the residential apartment or office

block.

4. Tenants of the office block are agents for withholding value added tax (VAT) and withholding rental

income.

5. The figures provided are quoted inclusive of VAT where applicable.

Required:

(i) Calculate the tax payable under the VAT and income tax obligations by KK Realtors for the month of

December 2022.

(ii) Show the withholding tax collected under the obligations in (b)(i) above, if any, as well as the net rent

income received by KK Realtors, as cash.

5a

Tax systems and policies

Tax planning

Professional practice in taxation

Explain THREE reasons why investment allowances as tax incentives have not achieved the intended objectives in

your country.

5b

Tax planning

Professional practice in taxation

Tax investigations

Tax risks are broadly classified into specific and generic categories.

Analyse TWO types of risks in each category.

5c

Taxation of business income and specialized business activities

Tax systems and policies

Johnson Shauri has not been maintaining proper books of accounts since the inception of his business in year 2019.

The following balances were obtained from the available business records for the four year period ended

31 December 2022:

| 31 December 2019 | 31 December 2020 | 31 December 2021 | 31 December 2022 | |

| Sh.“000” | Sh.“000” | Sh.“000” | Sh.“000” | |

| Leasehold property | 11,760 | 11,760 | 11,760 | 11,760 |

| Motor vehicles | 5,040 | 4,720 | 9,360 | 10,760 |

| Furniture | 864 | 864 | 864 | 864 |

| Bank overdraft | 1,288 | 1,400 | 1,210 | 1,115 |

| Loss on sale of investment | - | 100 | - | - |

| Accounts receivable | 432 | 504 | 408 | 600 |

| Mortgage loan | 2,080 | 1,840 | 1,620 | 1,500 |

| Inventory | 620 | 572 | 482 | 520 |

| Computers | 620 | 720 | 840 | 720 |

| Bank account | 240 | 268 | 272 | 286 |

| Personal clothes and effects | 60 | 80 | 100 | 120 |

The following additional information was obtained:

- Drawings of goods and provision for taxation for the year 2019 were Sh.600,000 and Sh.360,000 respectively and has been accumulating at a rate of 10% annually.

- Capital allowances were agreed at a total of Sh.920,000 for each of the four years.

- Donations to a political party in the year 2020 amounted to Sh.142,000.

- Gifts from relatives for the year 2021 were Sh.840,000.

- Contingent liability in respect of a pending court case in the year 2022 was Sh.1,000,000.

- Rent paid on behalf of a close friend was Sh.605,000 in the year 2022.

- Living expenses were estimated at Sh.800,000 in the year 2019 and had been increasing at the rate of 15% cumulatively each year.

Required:

(i) Compute the taxable income or loss of Johnson Shauri for the three-year period ended 31 December 2020, 2021

and 2022.

(ii) Summarise THREE specific actions that a tax practitioner could undertake upon discovery of an irregularity in the

client’s business.

Sign in with Google

Sign in with Google

Want to join the discussion?

Log in to post comments and interact with tutors.

Login to Comment